Eminent Domain and the Displacement of Black Communities

Eminent Domain and the Displacement of Black Communities More than a century ago, before there was today’s Prince William Forest Park, there was a community

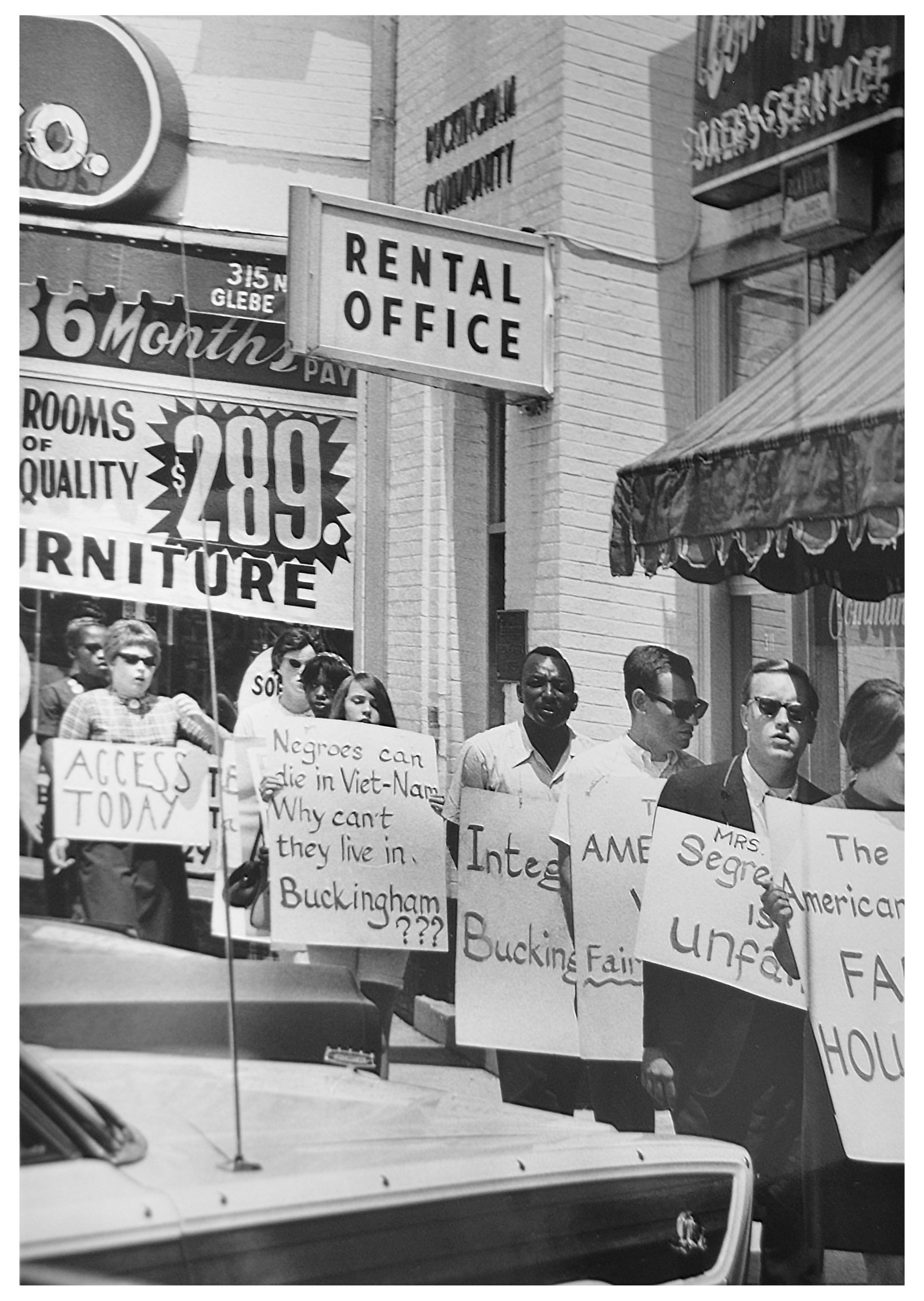

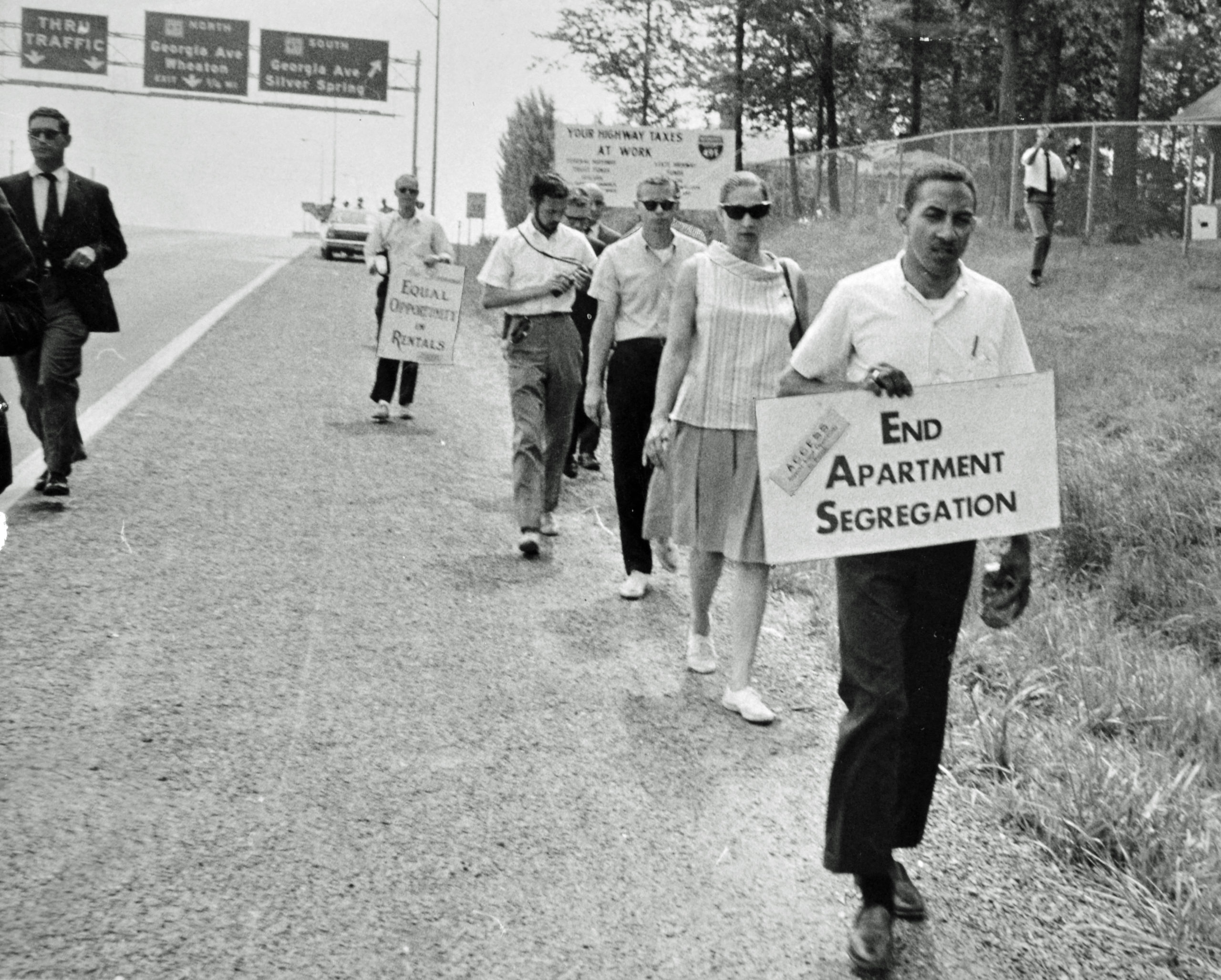

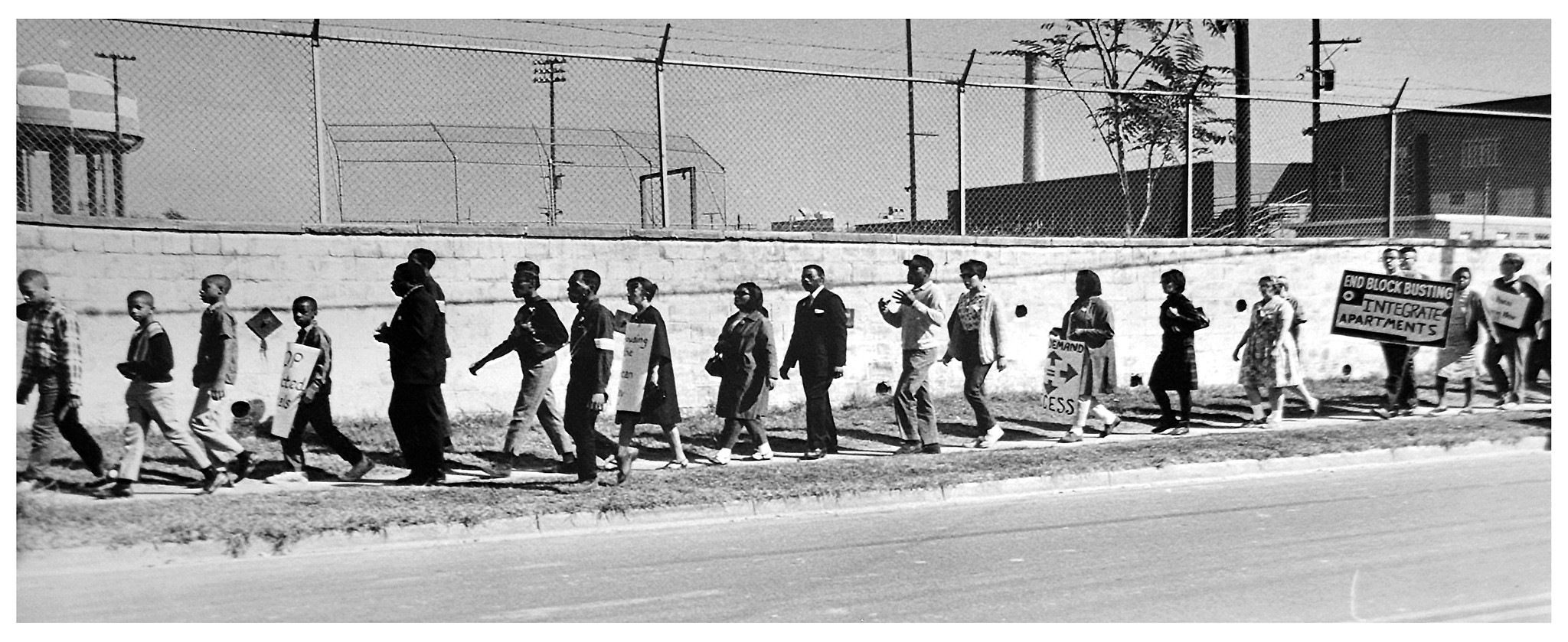

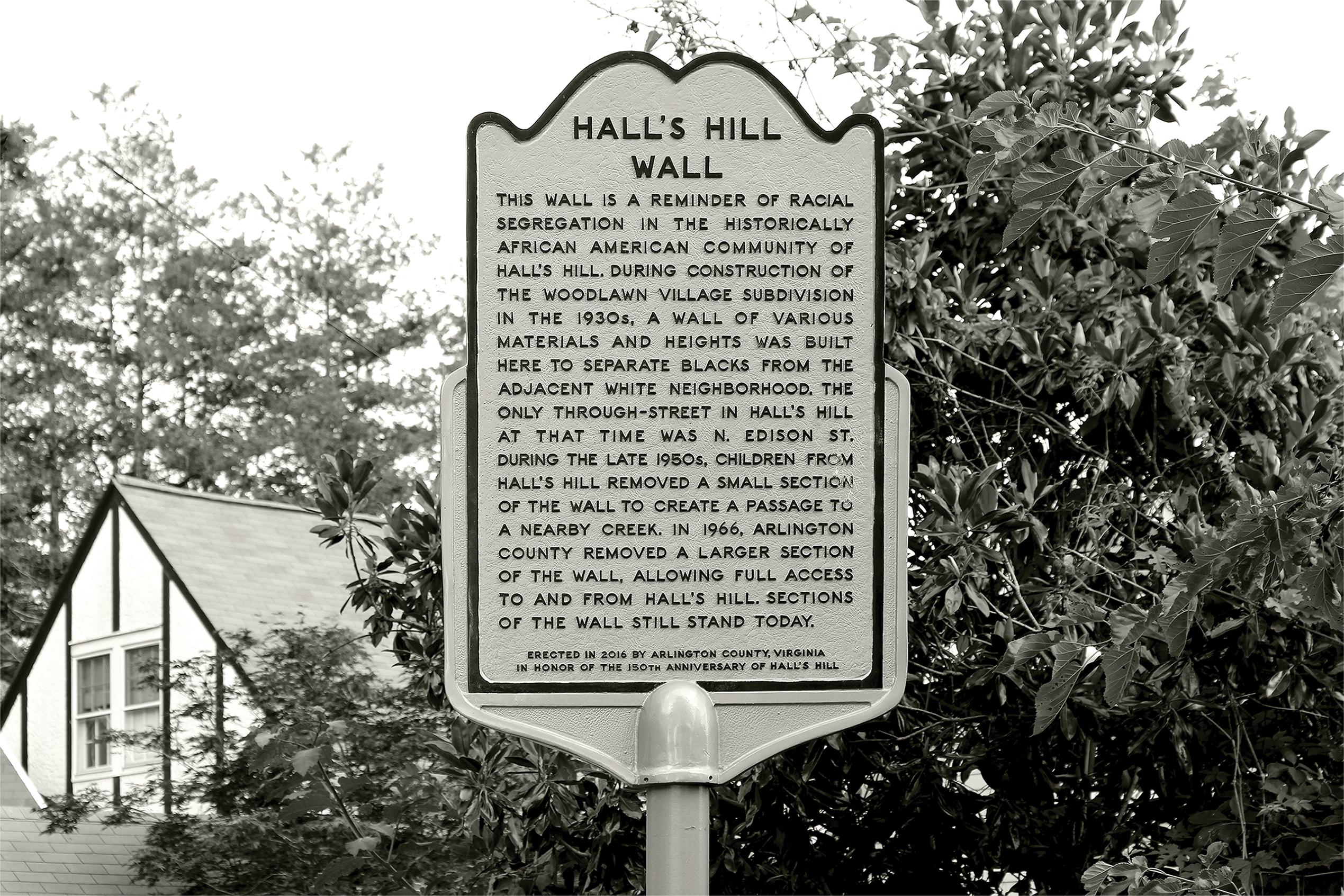

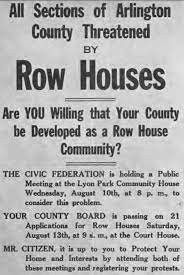

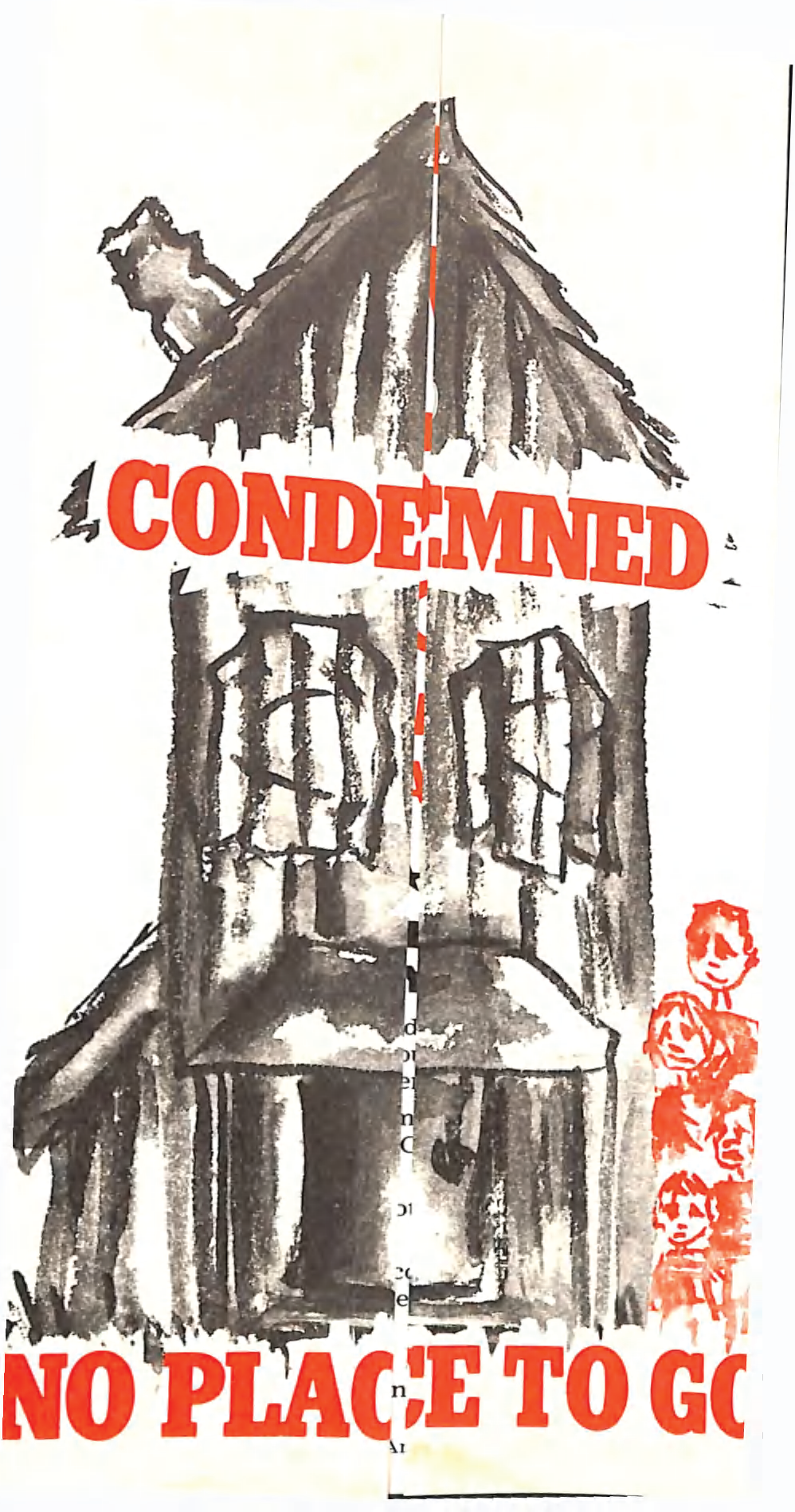

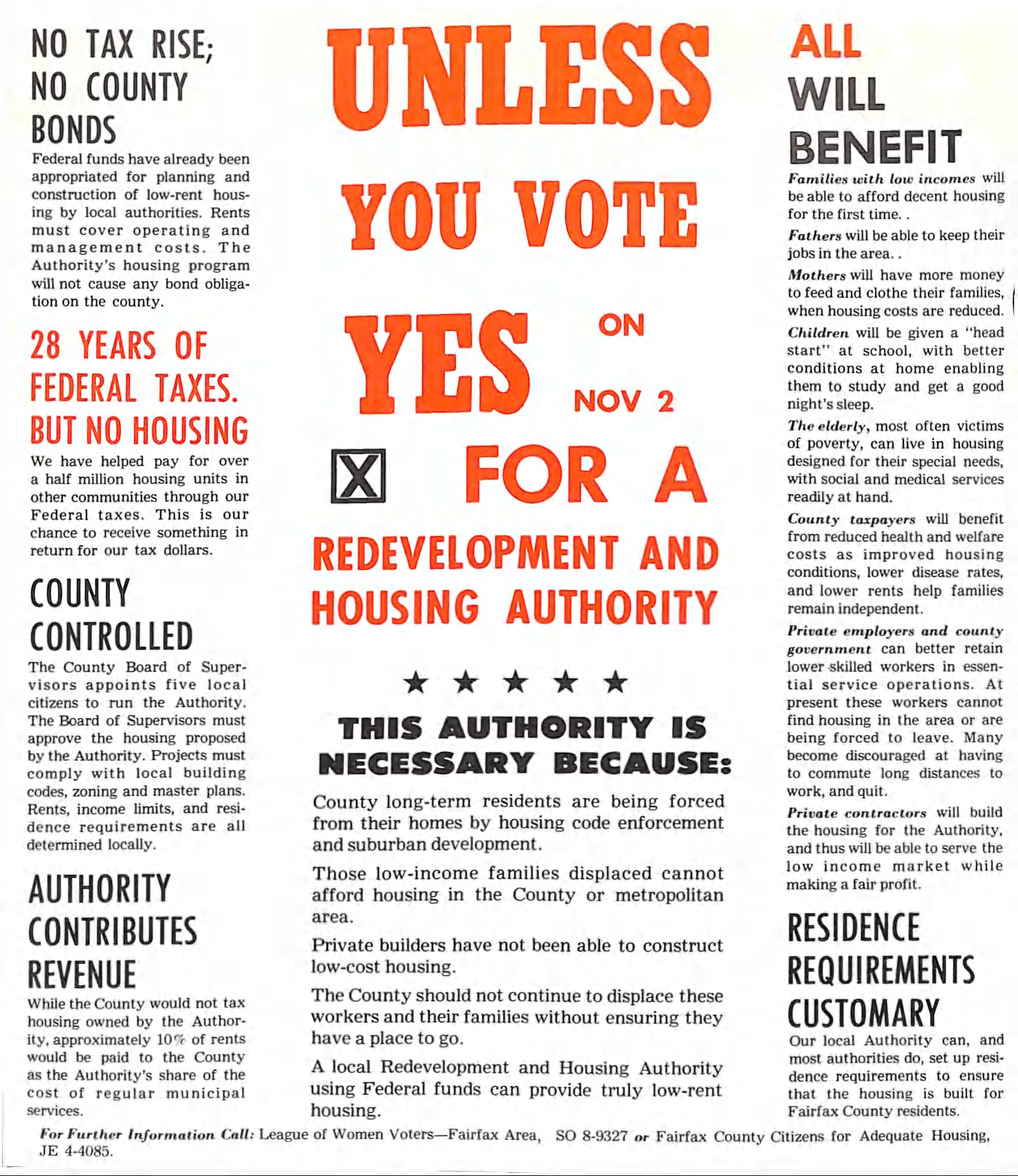

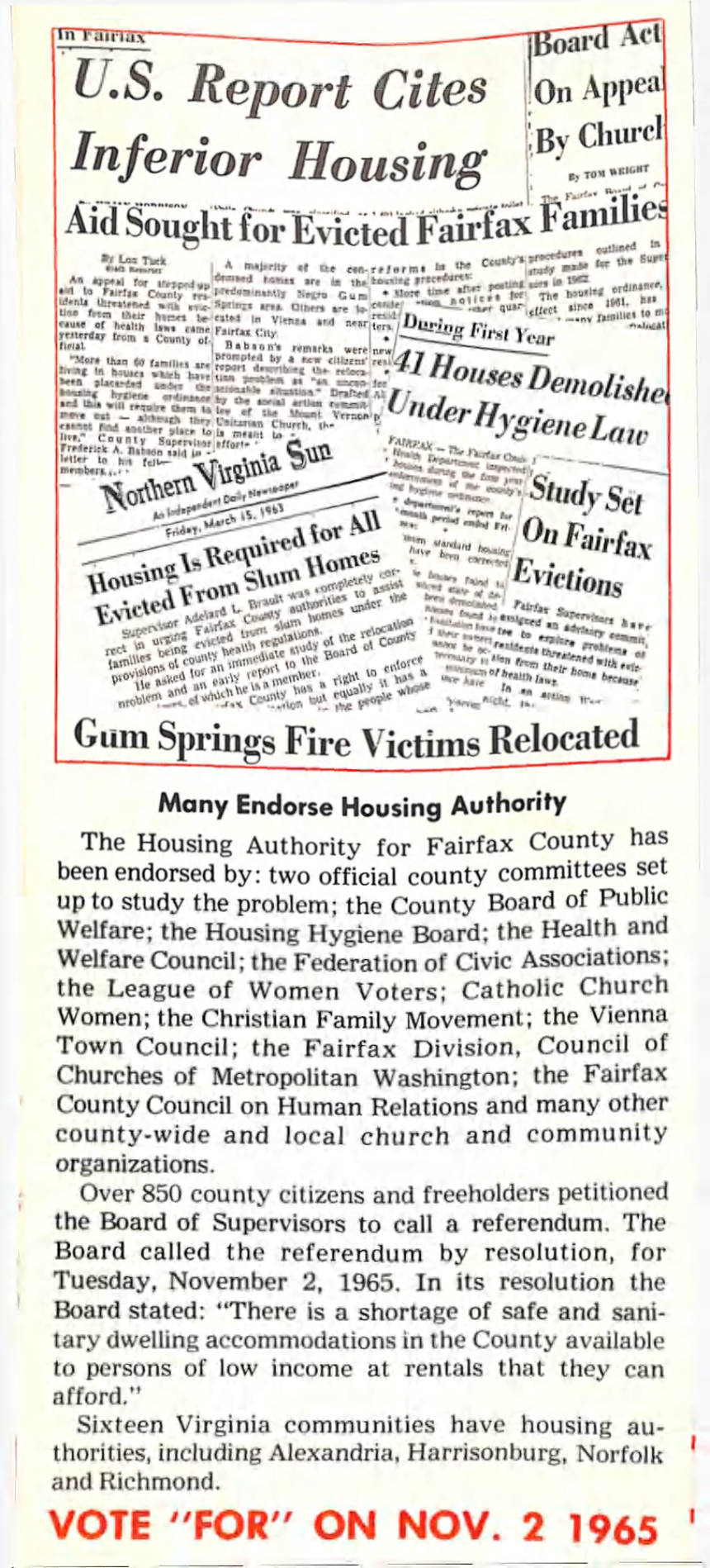

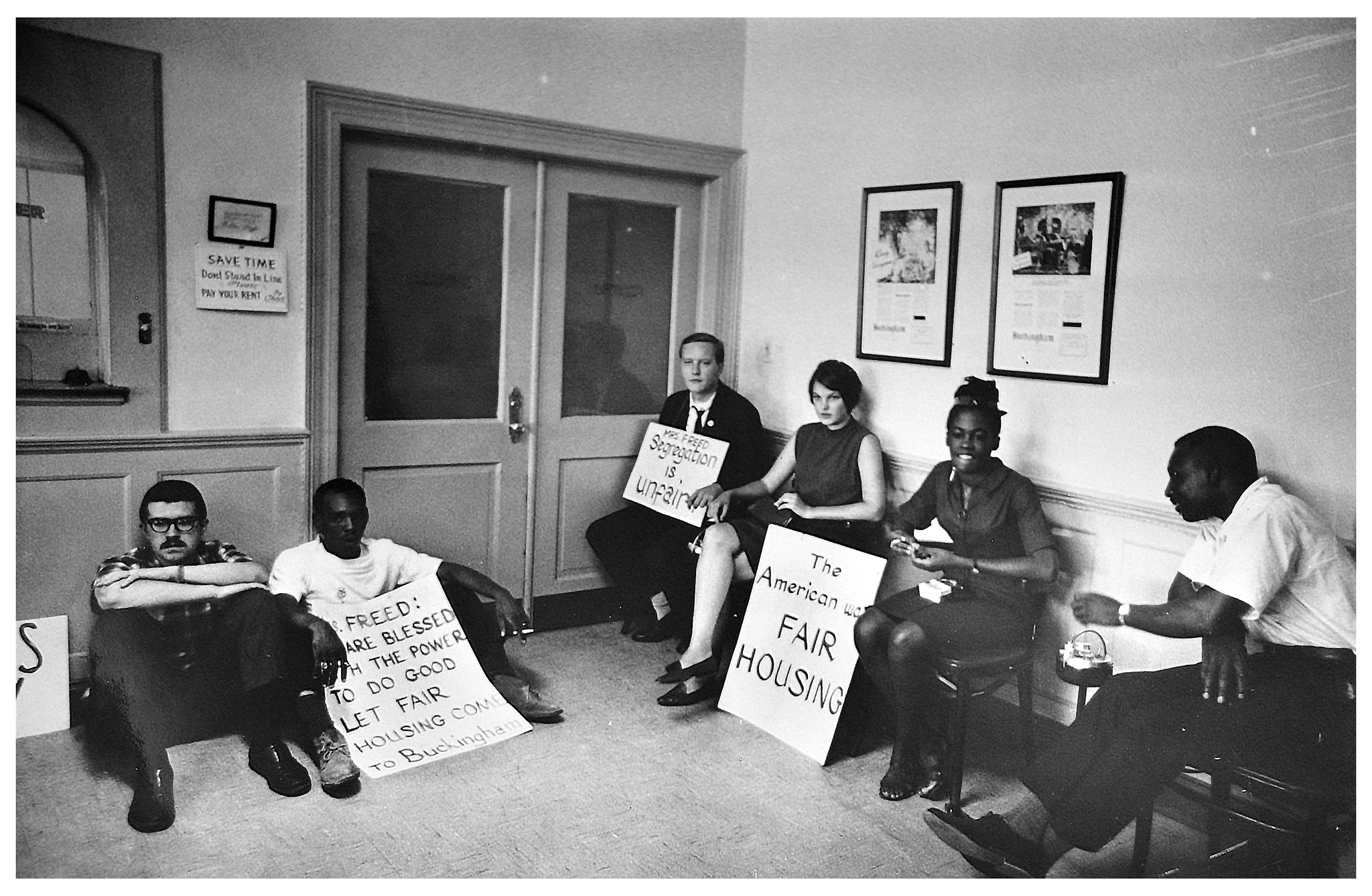

Housing Segregation: Nowhere to Live

In 2016, Chris Fullman closed on his house in Richmond’s Lakeside. After signing the papers, his closing attorney handed over a copy of the covenants